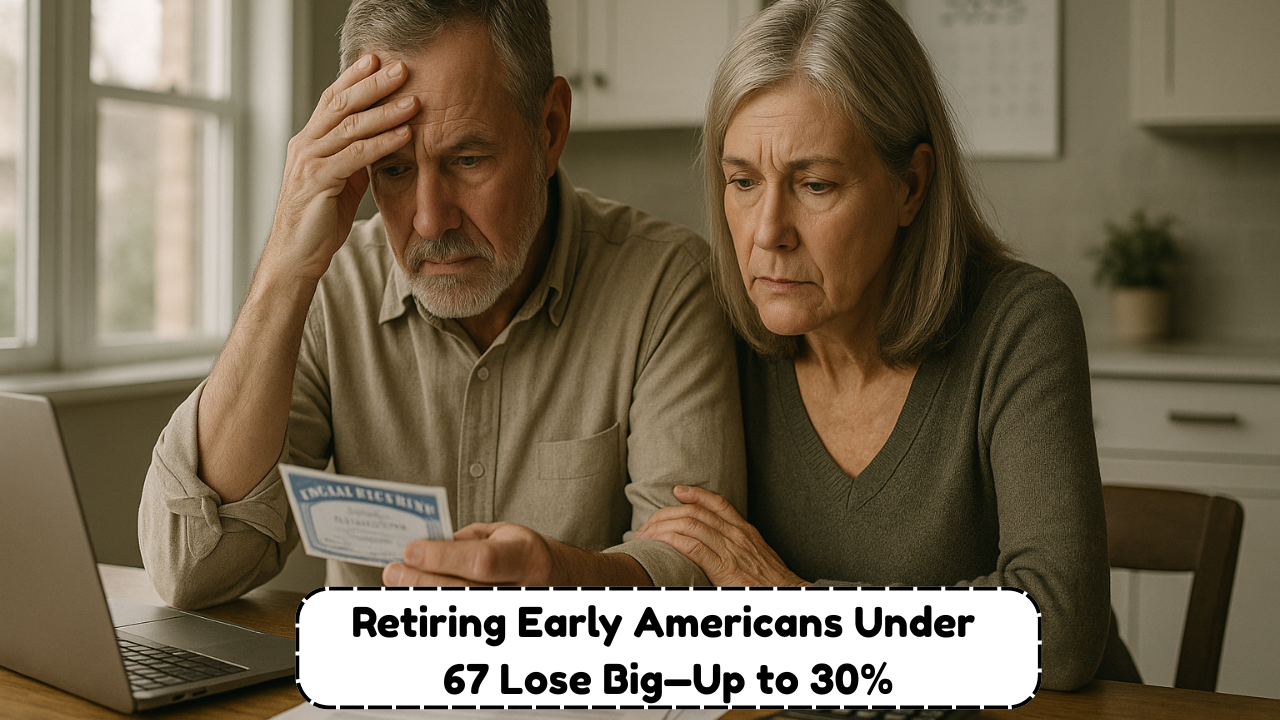

Millions of Americans born after 1960 are facing a harsh reality: if they choose to retire at age 62 — the earliest possible age to claim Social Security — they will see up to a 30% permanent reduction in their monthly benefits. This change is due to the gradual increase in the Social Security Full Retirement Age (FRA), which is scheduled to reach 67 for those born in 1960 or later.

As retirement costs soar and life expectancy continues to rise, understanding how early retirement impacts your long-term financial health is more crucial than ever. This article breaks down the new rules, the financial consequences of early claims, and how you can protect your retirement income.

What Is Full Retirement Age (FRA) and Why Is It Changing?

The Full Retirement Age (FRA) is the age at which you become eligible to receive 100% of your Social Security retirement benefit. FRA used to be 65 for decades, but legislation passed in the 1980s gradually raised it to accommodate longer life spans and ease financial pressure on the Social Security system.

FRA Changes by Year of Birth

| Year of Birth | Full Retirement Age (FRA) |

|---|---|

| 1954 or earlier | 66 |

| 1955 | 66 and 2 months |

| 1956 | 66 and 4 months |

| 1957 | 66 and 6 months |

| 1958 | 66 and 8 months |

| 1959 | 66 and 10 months |

| 1960 or later | 67 |

Anyone born after 1960 will need to wait until age 67 to receive full retirement benefits — and will face steep cuts if retiring earlier.

Retiring at 62? Expect a 30% Benefit Reduction

Although age 62 is still the earliest age at which Americans can claim Social Security retirement, doing so comes at a significant cost. For those with an FRA of 67, retiring at 62 results in a permanent 30% reduction in monthly benefits.

How Early Retirement Reduces Benefits

| Retirement Age | Percentage of Full Benefit (FRA 67) | Monthly Loss |

|---|---|---|

| 62 | 70% | -30% |

| 63 | 75% | -25% |

| 64 | 80% | -20% |

| 65 | 86.7% | -13.3% |

| 66 | 93.3% | -6.7% |

| 67 | 100% | No Reduction |

Choosing to retire early locks in a lower benefit amount for life. For example, someone eligible for $2,000/month at 67 would receive only $1,400/month if they start collecting at 62.

Why Full Retirement Age Is Increasing

The increase in the full retirement age is part of a broader effort to stabilize the Social Security Trust Fund, which has faced solvency issues due to:

- Longer life expectancy

- A growing number of retirees vs. workers

- Declining birth rates and slower workforce growth

Raising the FRA helps reduce the strain on the system by encouraging people to work longer and delaying benefit payouts.

How This Affects Americans Born After 1960

If you were born in 1960 or later, you now fall under the new retirement age of 67. Retiring before that age — even by a few years — will have a major impact on the total income you receive throughout retirement.

Long-Term Impact Example

| Scenario | Total Benefits Over 20 Years (Est.) |

|---|---|

| Retire at 67 | $480,000 ($2,000/month x 240 months) |

| Retire at 62 (30% cut) | $336,000 ($1,400/month x 240 months) |

| Difference | -$144,000 |

Over the course of 20 years, retiring at 62 instead of 67 could cost you more than $140,000 in lost benefits.

What Are Your Options to Offset the Reduction?

While early retirement is tempting, especially for those in physically demanding jobs or poor health, it’s essential to explore all your options before filing at 62.

Strategies to Maximize Your Benefits

- Work Longer: Each year you delay claiming up to age 70 adds about 8% to your benefit.

- Delay Social Security: Waiting until 70 can increase benefits by up to 24% over FRA.

- Use Other Income First: Tap into savings or investments to delay Social Security.

- Consider Spousal Benefits: Coordinating with a spouse can optimize household income.

- Work Part-Time in Retirement: Supplement income while letting benefits grow.

The longer you wait to claim, the more financial security you’ll have in your later years.

State Wise Social Security Full Retirement Age Set to Hit 67

In a critical update from the Social Security Administration (SSA), Americans born in 1960 or later will see a permanent 30% reduction in their monthly benefits if they choose to retire early at age 62. This comes as the Full Retirement Age (FRA) officially settles at 67 for this cohort, following phased increases over previous decades.

The decision affects millions planning early retirement and is part of the SSA’s strategy to maintain benefit sustainability while encouraging longer workforce participation. Here’s a state-wise projection of affected early retirees and FRA enforcement timeline:

| State | Est. Affected Retirees (Born 1960+) | Early Retirement Loss (%) | Full Retirement Age | Local SSA Outreach Efforts |

|---|---|---|---|---|

| California | 325,000 | 30% | 67 | Monthly webinars & clinics |

| Texas | 289,000 | 30% | 67 | Rural benefit advisories |

| Florida | 265,000 | 30% | 67 | In-person sessions for seniors |

| New York | 233,000 | 30% | 67 | SSA mailer campaigns |

| Pennsylvania | 194,000 | 30% | 67 | Veteran support outreach |

| Illinois | 165,000 | 30% | 67 | Bilingual SSA assistance |

| Ohio | 157,000 | 30% | 67 | Early retirement warning drive |

| Georgia | 151,000 | 30% | 67 | Pre-retirement workshops |

| North Carolina | 149,000 | 30% | 67 | County-level consultations |

| Michigan | 143,000 | 30% | 67 | Senior centers on alert |

| Arizona | 118,000 | 30% | 67 | SSA volunteer clinics |

| Washington | 112,000 | 30% | 67 | Digital application training |

| New Jersey | 108,000 | 30% | 67 | Retirement planning seminars |

| Virginia | 105,000 | 30% | 67 | Statewide SSA info push |

| Massachusetts | 101,000 | 30% | 67 | Financial planning guidance |

| Remaining States | 1,500,000+ | 30% | 67 | Local SSA coordination teams |

Important: Claiming Social Security at 62 locks in the reduced rate for life, unless withdrawn within 12 months and repaid in full. Americans are encouraged to use the MySSA portal to estimate their personalized benefit impacts and explore alternative retirement ages.

Should You Still Consider Retiring at 62?

It depends on your health, income needs, and life expectancy. For some, retiring at 62 is the best option, even with the penalty — especially if they have limited income sources or serious health concerns.

Reasons People Still Choose to Retire at 62

| Reason | Explanation |

|---|---|

| Poor Health | May not live long enough to benefit from delaying |

| Job Burnout | Physically or mentally unable to continue working |

| No Other Income Sources | Need to access cash flow immediately |

| Personal Preference | Want more time to enjoy retirement |

| Family History of Short Life | Expectancy impacts decision-making |

Every situation is unique, so retirement timing should be based on personal and financial realities.

Future Changes to Watch: Is FRA Going Higher?

With Social Security funding concerns continuing to mount, some lawmakers have floated proposals to raise the FRA even further — potentially to 68 or 70 in future decades. While nothing has been confirmed, younger workers should be prepared for the possibility.

Potential Policy Proposals

- Raise FRA to 68 or 70 for future generations

- Means testing for wealthy retirees

- Lower cost-of-living adjustments (COLAs)

- Increase in payroll taxes

Staying informed about Social Security reform debates will be critical for anyone under age 50.

For Americans born after 1960, retiring at 62 comes at a serious cost — a 30% reduction in monthly Social Security income for life. While early retirement may suit some, delaying even a few years can significantly improve your long-term financial stability.

Understanding how full retirement age works, calculating the potential losses, and planning accordingly can make the difference between struggling in retirement and enjoying it comfortably.

Frequently Asked Questions (FAQs)

What is full retirement age (FRA) for people born after 1960?

For anyone born in 1960 or later, the FRA is 67. This is the age at which you receive 100% of your Social Security benefits.

How much do I lose if I retire at 62?

You will receive only 70% of your full benefit, meaning a permanent 30% reduction in monthly payments.

Is it better to wait until 70 to collect Social Security?

Yes, if possible. Waiting until 70 can increase your benefit by up to 24% over what you’d get at FRA.

Can I work while collecting Social Security at 62?

Yes, but your benefits may be temporarily reduced if you earn over the annual income limit. These reductions are returned in later years.

Will the retirement age increase again in the future?

It’s possible. Some proposals suggest increasing the FRA to 68 or 70, but no laws have been passed yet.

Does this affect Medicare eligibility?

No. Medicare eligibility remains at age 65, regardless of when you claim Social Security.

Should I consult a financial advisor before deciding?

Absolutely. A financial advisor can help analyze your retirement needs and guide you on when to claim benefits.

Where can I check my Social Security benefit estimate?

You can view your personalized benefits statement online at ssa.gov.